More inflation coming soon

Monetary policy is out of control

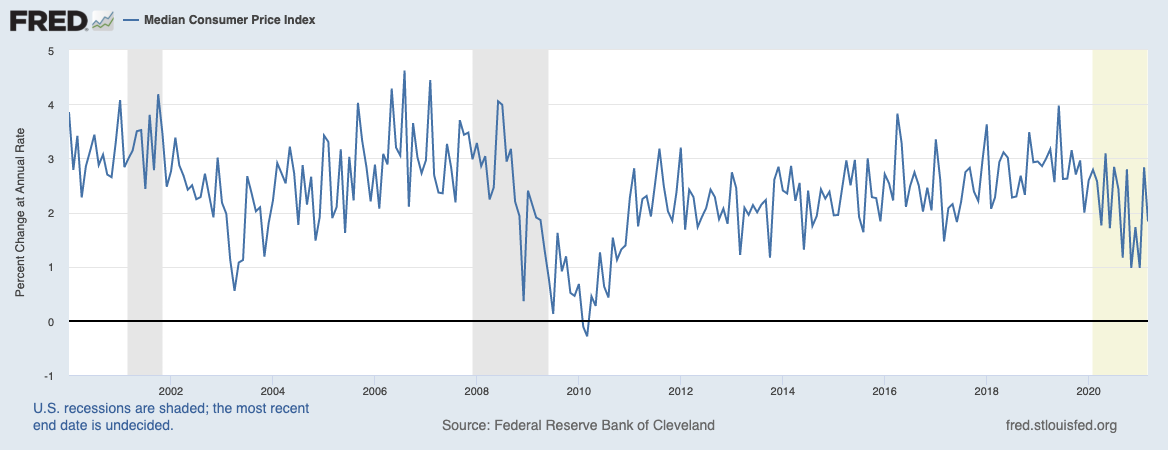

We are assured by the dubious financial media and executive branch officials that inflation, should any materialize, will be short-lived and manageable. And why not? Monetary hawks consistently predicted inflation throughout the 2010s, including early in the decade during intense phases of “quantitative easing”—a fancy term for the Fed creating new dollars out of thin air to buy up government and private debt. But as the chart below indicates, inflation, at least as measured by the Consumer Price Index, remained mostly in the two to three percent range for most of the 2010s—tame by historical standards.

But that was child’s play compared to the amount of dollar creation going on today. While headlines focus on improbable vows by the Fed and Treasury officials to keep rates low through 2023, the real action is in open market operations—printing dollars, at least electronic ones, to buy enormous amounts of debt. The chart below shows the degree of the activity, and it is without precedent in U.S. monetary history. The open spigot after the 2008-2009 financial crisis seems like a drop in the bucket compared to the fire sale on dollars since March 2020.

Furthermore, this trend is likely to continue. How can it not? Higher prices are already here, and reckless, speculative bubbles like Bitcoin, SPACs and coastal real estate abound. There are murmurs about whether the Fed may “taper” its binge come fall. Certainly it should, but the Fed isn’t just creating dollars to buy mortgages and existing government debt. It is also creating dollars to buy the insane amount of new debt the government is issuing—another trend with no end in sight.

The federal budget deficits for 2020 and 2021 were merely supposed to be about $1 trillion each (a level which a decade earlier sparked the Tea Party). Depending on whose accounting you trust, the federal government has spent an additional $6 trillion on relief related to the coronavirus pandemic.

While the pandemic ends, the spending binge persists. The administration and Congress favor significant additional expenditures if they can be vaguely linked to the pandemic. For example, some want to spend more than two trillion additional dollars on infrastructure that isn’t really related to the pandemic, and includes items like child care that isn’t really related to infrastructure. And it doesn’t end there. Work is already under way on the budget for Fiscal Year 2022, which begins this October 1. Progressives in Congress who have been on a legislative winning streak see this as a once-in-a-generation opportunity to raise baseline spending dramatically.

More spending means bigger deficits and more dollar creation as the Fed buys bonds issued by the Treasury that the market doesn’t want.

These factors alone would only be mildly alarming if the long-term outlook for real private sector growth was good. But it isn’t. Washington is determined to raise taxes to pretend to pay for some of the massive spending it has undertaken. Behind the scenes and largely unreported is the installation of progressive staff throughout the administration who will bring back the death-by-1000-cuts regulations that marked the lost decade of economic growth after 2008. Also back from that era is a shrinkage in workforce even amid low unemployment rates as people are given extended unemployment and other benefits that create a rational choice not to work.

Of the many new taxes suggested, a proposal to double the capital gains tax on investments would particularly stifle new business avenues for all of the newly created dollars sloshing around.

What this all means is that there likely will be too many dollars chasing too few goods and services—the standard definition of inflation. Previous loose monetary policy, especially during the 2010s, occurred as Europe and East Asia (ex-China) stagnated, especially in their currencies, keeping the dollar relatively strong. That plus unwisely deciding to buy more and more cheap manufactured goods from China masked inflation—although it has existed in the housing market since 2010.

None of these previous mitigating factors is likely to stave off inflation today. The growth in money supply is too big and seemingly too politically difficult to stop. Outside of travel, East Asia has bounced back and Europe will follow. Inflation, the insidious tax on everything, which hurts the poor most and discourages saving and hard work, is probably here to stay.